Article by

Lee and Stuart

Lee Stancer & Stuart Allen – Kobb Interiors Ltd

Lee Stancer and Stuart Allen are the directors of Kobb Interiors Ltd, a Harrogate-based interiors company specialising in the design and installation of bespoke kitchens, bedrooms, home offices, and shutters. With a shared passion for craftsmanship and modern, thoughtfully designed spaces, they combine creative vision with practical expertise to deliver high-quality, tailored interiors.

Lee focuses on design, client experience, and brand direction, bringing a warm, contemporary style to each project. Stuart complements this with strong technical knowledge and project delivery, ensuring every detail is executed to the highest standard.

Together, they have built Kobb Interiors into a trusted destination showroom, offering premium products including solid surfaces as a Cosentino Elite partner, as well as leading appliance, tap, and furniture solutions. Their collaborative approach ensures every space is both beautiful and functional, designed to enhance the way their clients live.

What if the true foundation of your new kitchen isn't the solid quartz worktop or the hand-painted cabinetry, but the quiet rhythm of a well-structured financial plan? It's a common tension. You desire a space that reflects your personal heritage, yet the weight of a long-term commitment can feel heavy. It's natural to worry about hidden costs or to feel a sense of confusion when trying to balance monthly affordability against the total interest paid over time.

Mastering the relationship between the loan amount and the term. allows you to bridge the gap between architectural ambition and financial clarity. Whether you're considering 0% interest-free finance for up to seven years or a flexible monthly plan at 4.9% APR, the right structure ensures your project remains a source of peace rather than pressure. This guide explores how to calibrate these financial levers to suit your lifestyle, providing a clear map of modern credit regulations and practical ways to secure your premium kitchen with absolute confidence.

Key Takeaways

- Master the fundamental architecture of finance by distinguishing between your project's total principal and the duration of your repayment schedule.

- Discover how adjusting the loan amount and the term. can make even the most ambitious bespoke kitchen design feel manageable and serene.

- Identify the ideal repayment window for your lifestyle, from high-impact short-term paths to the popular medium-term balance for fitted bedrooms and bathrooms.

- Learn why aligning your investment with Harrogate and York property values ensures your home renovation serves as a lasting, purposeful asset.

- Gain clarity on the transparent, customized finance solutions available through our partnership with Novuna Personal Finance.

The Architecture of Finance: Defining the Loan Amount and the Term

Every masterpiece begins with a structural frame. In the context of a home renovation, that frame is built upon two distinct pillars: the total capital borrowed and the time allocated to repay it. Mastering the relationship between the loan amount and the term. allows you to approach your project with the same discernment you apply to selecting a palette of materials. It transforms a complex financial decision into a rhythmic, manageable flow that preserves the serenity of your daily life. By understanding these variables, you move from a place of uncertainty to one of quiet confidence.

To better understand how these variables interact to shape your monthly investment, watch this helpful video:

The Principal: More Than Just a Number

The principal represents the heart of your creative vision. It encompasses the tactile reality of your space, from the cool, organic touch of Silestone worktops to the refined utility of Quooker boiling water taps. By establishing a clear loan amount at the outset, you create a purposeful ceiling for your project scope. This boundary prevents the subtle drift of scope creep, ensuring that every detail, from bespoke cabinetry to integrated Smeg appliances, remains within a defined financial landscape. The principal is the foundational investment in your home sanctuary.

The Term: Curating Your Repayment Journey

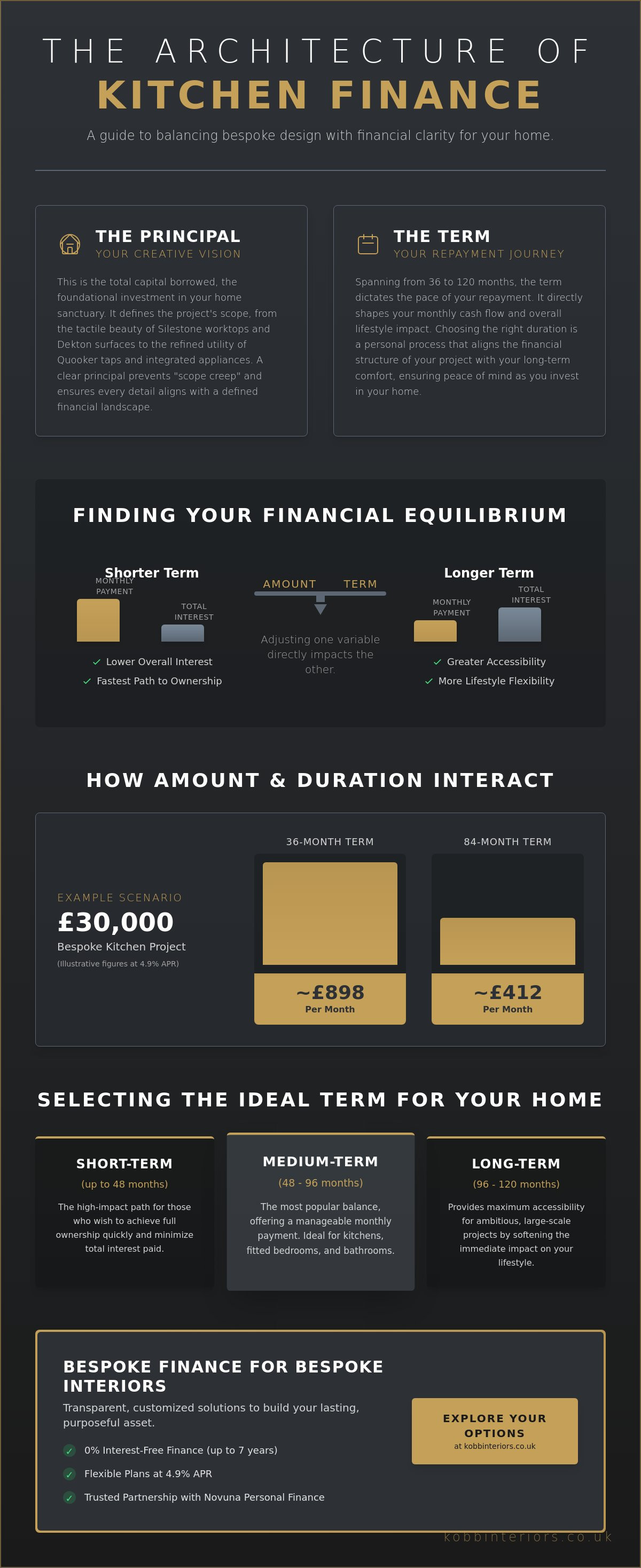

If the principal is the space itself, the term is the timeline of ownership for your new interior. Usually spanning between 36 and 120 months, the term dictates the pace of your repayment journey and directly shapes your monthly cash flow. A shorter term is the fastest route to full ownership. It often results in lower overall interest, though it requires a more significant monthly commitment. Conversely, extending the duration can make a premium kitchen more accessible by softening the immediate impact on your lifestyle. Finding the right balance between the loan amount and the term. is a deeply personal process that aligns your financial structure with your long-term comfort.

Each payment you make is a deliberate step toward equilibrium. An amortization schedule provides a transparent view of this progression, detailing how each contribution is divided between the principal and the interest. This clarity is essential for maintaining peace of mind, especially as the UK government modernizes credit regulations to provide consumers with better-timed information. By choosing a structure that mirrors your household's rhythm, you ensure the beauty of your new space is supported by a steady, reliable hand. Explore our finance options to see how these variables can be tailored to your specific Harrogate or York residence.

Calculating Your Investment: How Amount and Duration Interact

Precision defines the most successful interiors. When you begin to shape your financial plan, you'll find that the loan amount and the term. operate in a constant state of flux; a change in one necessitates an adjustment in the other. A higher loan amount naturally increases the monthly commitment if the duration remains static. Conversely, extending the period can make a premium bespoke kitchen more accessible by diluting the monthly cost across a broader timeline. The Annual Percentage Rate (APR) acts as the essential bridge between these two variables, determining the final cost of your project.

The Impact of the Loan Amount on Monthly Outgoings

Selecting between a £15,000 and a £30,000 investment shifts the monthly requirement significantly. While a lower figure might feel safer, a higher amount often allows for the inclusion of materials that offer superior longevity and tactile beauty. Choosing Dekton for your worktops or opting for hand-painted cabinetry shouldn't be viewed as a mere expense. Instead, it's a quality investment in your Harrogate property that enhances both functional utility and long-term value. When calculating your loan payments, focus on the "sweet spot" where project quality meets your monthly comfort level.

How the Term Influences Total Interest Paid

While extending your term lowers the monthly outgoings, it's useful to remember that a longer duration increases the total amount repayable. For a standard kitchen project, a 3-year term offers the fastest route to full ownership and minimizes interest costs. A 5-year term, however, provides a more spacious budget for daily living. There is a distinct psychological benefit to a shorter term for those who value the feeling of being debt-free sooner. It creates a sense of completion that mirrors the final handover of your finished space. If you're curious about how these numbers translate into real-world designs, explore our project gallery to see the level of craftsmanship your investment secures.

Selecting a Loan Term: Finding Equilibrium for Your Yorkshire Home

Achieving a sense of equilibrium in your Yorkshire home requires more than just aesthetic balance; it demands a financial structure that breathes with your lifestyle. The relationship between the loan amount and the term. is the mechanism that allows you to calibrate this breath. As you look toward your financial goals for 2026, selecting the right duration becomes a purposeful act of design. It's about finding the point where your desire for a premium environment meets the reality of your monthly rhythm. Whether you're refining a sanctuary in Harrogate or a heritage space in York, the timeline you choose defines your journey toward full ownership.

Short-Term Commitments for Swift Completion

Choosing a term of one to three years is a path often favored by those who value rapid progression. It's an ideal choice for high earners or homeowners expecting specific liquidity, such as an annual bonus, who wish to clear the balance quickly while already enjoying their new space. While the monthly impact is higher, the reward is a significantly lower total interest cost and the psychological satisfaction of a swift project pay-off. Ownership is immediate. The transition from a financed project to a fully realized asset happens with a decisive, steady hand, allowing you to move forward with total financial freedom.

The Grace of Long-Term Financing

There is a quiet dignity in choosing a path that preserves your daily liquidity while still allowing for the finest materials to grace your home. A longer term, ranging from seven to ten years, maximizes monthly serenity. It allows for a larger project scope today without a heavy immediate capital drain. By spreading the investment, you can secure the "dream" specification, perhaps including bespoke fitted bedrooms or an expansive media unit, while maintaining a stable, fixed monthly payment. In an evolving economy, this stability is a form of future-proofing. It ensures your home remains a sanctuary of comfort rather than a source of pressure.

For many residents in North Yorkshire, the medium-term window of four to six years represents the most popular balance. It offers a measured pace that fits comfortably within a standard household budget while keeping the total interest manageable. This duration is particularly effective for projects that bridge multiple rooms, ensuring a cohesive design language across your interior. By aligning your choice with your personal comfort level, you ensure that the beauty of your surroundings is matched by the clarity of your financial plan. If you're ready to discuss how these durations might apply to your vision, our team is here to listen at our Harrogate showroom.

Strategic Budgeting for Bespoke Interiors in Harrogate and York

Living in North Yorkshire presents a specific set of opportunities for homeowners. Property values in Harrogate, York, and Wetherby often justify a more significant investment in interior architecture compared to other regions. When you evaluate the loan amount and the term., it's helpful to view these figures through the lens of property appreciation. A well-executed renovation doesn't just improve your daily life; it secures the future value of your home. Aligning your borrowing with the anticipated value-add ensures that your project is a purposeful financial move rather than a mere expense. It's about creating a sanctuary that respects the market reality of your surroundings.

Investment vs. Expense in Local Property Markets

In the prestigious neighborhoods of Harrogate and Wetherby, bespoke kitchens from heritage brands like 1909 are recognized as hallmarks of quality. The right loan amount ensures you don't under-spec a high-value property with materials that feel out of place. A luxury home deserves a luxury finish. It's essential to match the quality of your kitchen to the prestige of your postcode to maintain a cohesive narrative of craft throughout the residence. By opting for a finance structure that supports high-end choices, you protect the integrity of your largest asset while enjoying the tactile beauty of custom cabinetry.

Holistic Project Costing

A successful project requires a comprehensive view of costs. Your loan amount should encompass more than just the cabinetry and worktops; it must include full project management, meticulous installation, and those final finishing touches. Integrating premium AEG or Smeg appliances from the start creates a seamless functional experience that pays dividends in daily convenience. We often recommend including a modest contingency within your funding to handle any unforeseen structural nuances with grace. This foresight ensures the journey from initial design to final handover remains calm and uninterrupted. You can explore our project gallery to see how these holistic details come together in real Yorkshire homes.

When you're ready to define the scope of your own transformation, you can book a design consultation with our Harrogate team to align your vision with a practical financial plan. We'll help you navigate the relationship between the loan amount and the term. to ensure your home renovation is as rewarding as it is beautiful.

Bespoke Finance for Bespoke Interiors: The Kobb Interiors Approach

At Kobb Interiors, we believe the financial architecture of a project should be as meticulously crafted as the cabinetry itself. Our partnership with Novuna Personal Finance allows us to offer solutions that are both flexible and transparent, ensuring your journey remains undisturbed by administrative friction. We begin with your vision—the color compositions, the physical surfaces, and the functional utility of the space—and then align the financial structure to your personal comfort level. By tailoring the loan amount and the term. to your unique requirements, we ensure that the beauty of your new environment is matched by a sense of absolute financial peace.

A fully managed project is a sensory experience that progresses with a refined, steady hand. From the initial layout of your home office to the final installation of plantation shutters, our team oversees every detail. This same level of care extends to your payment plan. It shouldn't feel like a generic transaction; it should feel like a curated component of your home's narrative. By integrating financial planning into the creative process, we remove the anxiety of long-term commitment and replace it with the quiet confidence of a well-executed plan. This holistic approach is what transforms a renovation into a sanctuary.

The Novuna Partnership: Why Clarity Matters

Clarity is the cornerstone of trust. For our clients across Harrogate and York, the application process is designed to be seamless and discreet. Through our partnership with Novuna, we provide fixed rates and clear repayment structures that protect you from the unpredictability of the wider market. This stability allows you to focus on the sensory details of your renovation, knowing that the foundation is secure. Every detail of your finance options is presented with the same precision we apply to a design blueprint, leaving no room for hidden costs or unexpected commitments. You're always in control of the pace and the total investment.

Your Next Steps Toward a Transformed Home

Your transformation begins with a conversation. We invite you to visit our Harrogate showroom, where you can experience the material quality of our work firsthand and discuss your project in a calm, unhurried atmosphere. Our designers are more than creators; they're trusted collaborators who help you balance the loan amount and the term. during the initial design phase. This integrated approach ensures that the final result is a sanctuary that serves both your aesthetic desires and your long-term financial goals. It's about finding that perfect equilibrium between the space you want and the life you live. When you're ready to take the first step toward a more purposeful home, contact Kobb Interiors to arrange your private consultation.

A Purposeful Path to Your Bespoke Sanctuary

True home transformation is an act of balance. It's a harmony between the physical structure of your space and the financial foundation that supports it. By calibrating the loan amount and the term. to your specific lifestyle, you create a path toward a home that serves as both a masterpiece of design and a sanctuary of peace. Our team brings over 40 years of local expertise to every Harrogate and York residence. We ensure a seamless transition from initial concept to final installation. Through our partnership with Novuna Personal Finance, we offer curated solutions that respect your budget while fulfilling your highest architectural ambitions.

This full project management approach guarantees that the process is as serene as the finished result. You deserve a space that reflects your heritage and supports your future. We invite you to explore our flexible finance options for your dream kitchen and begin your journey with confidence. Your vision is within reach, supported by a steady hand and a clear, manageable plan.

Frequently Asked Questions

How do I decide between a higher loan amount and a longer term?

Calibrating your investment involves weighing the tactile quality of your materials against your monthly comfort. A higher principal allows for the inclusion of premium elements like 1909 cabinetry or Dekton surfaces, which enhance your property's value. Choosing a longer duration ensures that this high-end specification doesn't disrupt your daily financial rhythm. Most homeowners find equilibrium by selecting a monthly payment that feels spacious while ensuring the project's material quality matches their home's prestige.

Can I change the loan term after the agreement has started?

No, the duration of your agreement is typically fixed once the contract is signed and the initial cooling-off period has passed. These fixed terms provide the stability of predictable monthly outgoings, which is essential for long-term financial peace. While you cannot usually extend the duration, many lenders allow you to make overpayments or settle the balance early. This flexibility helps you manage your commitment if your financial circumstances change during the life of the loan.

What is the maximum loan amount available for a bespoke kitchen in 2026?

Verified industry data from May 2026 indicates that 0% interest-free finance is frequently capped at £30,000 for terms up to seven years. For more expansive projects that require a larger principal, interest-bearing loans often offer higher ceilings based on individual lender criteria. It's essential to discuss your specific vision with our team so we can help you understand how the loan amount and the term. can be structured to suit your project's unique scale.

How does the loan amount and the term affect my credit score?

Every credit agreement influences your financial profile through the hard inquiry performed during the application and the subsequent record of your monthly repayments. The relationship between the loan amount and the term. determines your debt-to-income ratio, a metric lenders use to assess your financial reliability. Maintaining a consistent, timely payment schedule over the agreed duration is a purposeful way to demonstrate stability. It can enhance your credit standing for future endeavors by showing disciplined financial management.

Are there penalties for paying off the loan amount before the term ends?

Many modern finance agreements, including those regulated under the 2026 Consumer Credit Act reforms, permit early settlement without significant penalties. Some Buy Now Pay Later schemes may require a small administrative fee, such as £29, if you clear the balance during the initial holiday period. It's always wise to review your specific Novuna agreement details. Settling early can often reduce the total interest you pay, providing a clear financial benefit for those who choose a swifter path to ownership.

Does the loan term include the time taken for kitchen installation?

Repayment periods generally commence only after the primary goods have been delivered or the installation has reached a significant milestone. This ensures you aren't paying for a space you cannot yet use as a sanctuary. While the design and project management phases happen beforehand, the clock on your agreement typically starts when the transformation of your home is well underway. This alignment between the physical progress of the work and your financial commitment supports a stress-free experience.

What happens if the project cost changes after the loan amount is agreed?

If the project scope expands after your finance is finalized, the additional cost is usually handled as a separate cash balance. The original agreement remains static to preserve the stability of your monthly payments and interest rates. This approach prevents the complexity of re-applying for credit mid-project. We recommend including a modest contingency in your initial budget to ensure that any subtle design refinements can be executed with a refined, steady hand without requiring new financial arrangements.

Can I combine a deposit with a loan to reduce the term?

Yes, providing a substantial initial deposit is a highly effective way to refine your financial commitment. By reducing the principal from the outset, you can often opt for a shorter duration or secure more modest monthly outgoings. This strategy allows you to invest in high-end functional utility, such as Quooker hot taps or integrated AEG appliances, while keeping the financed portion of the project light. It's a disciplined way to balance immediate capital with long-term cash flow.

Finance Available

* Kobb Interiors Ltd is an Introducer Appointed Representative of Ideal Sales Solutions Ltd, t/a Ideal4Finance. Ideal Sales Solutions Ltd is a credit broker and not a lender (FRN 703401). Finance available subject to status. The rate offered is always provisional and will depend upon your personal circumstances, the loan amount and the term.